22/02/2024

The delays in the supply of Western weapons, exacerbated by a deadlock in the US over the approval of the aid to Ukraine, have introduced a sense of urgency for Ukraine to mobilise its internal resources for military production. Moreover, as the hopes for a swift victory have faded and the spectrum of a protracted war has become evident, the question of transforming the Ukrainian economy to a war model becomes imperative.

It is stunning, but after two years of war, the Ukrainian economy has not (yet) become a war economy. The central bank and the government have implemented a range of measures, but their scope and size remain insufficient for the war challenge. State defence expenses increased several times but are still below the needs of the army and available production capacity. According to estimates, only half of the capacity of the defence industry was used in 2023. There are objective reasons for the weak production, like the destruction of some production sites and shortages of workers. But the low volume of state procurement is the major impediment.

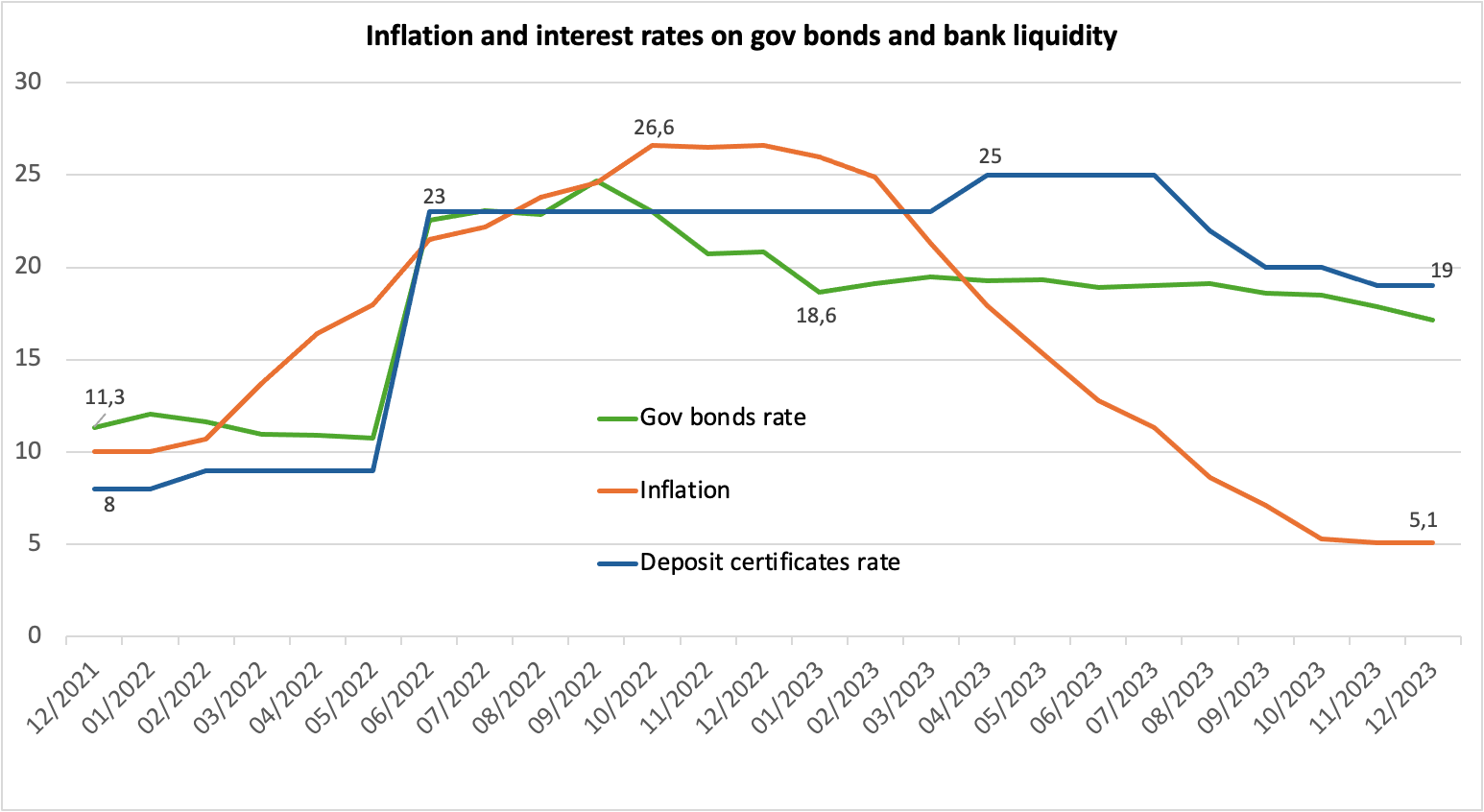

The truth is that the Ukrainian state does not have enough money to finance defence procurement. This limitation, however, is partially self-inflicted and there are various resources that can be mobilised. More alignment of the monetary policy with the needs of the war would be particularly helpful. The Ukrainian central bank (NBU) was very effective at the beginning of the war when it introduced a range of emergency measures that prevented a banking and currency meltdown (notably, capital and FX controls). Its later policies, however, were less supportive of the war economy. In June 2022, the central bank massively increased its main policy rate from 10 per cent to 25 per cent, motivating it by the need to contain inflation. On top of it, the NBU has tied the rate of remuneration of bank liquidity (the so-called deposit certificates) at minus two per cent points of the policy rate, so that banks could get risk-free 23 per cent on their liquidity. Logically, they were not eager to lend to business at rates lower than that, while business was not prepared to pay such exorbitant rates. This was one of the main reasons behind the stagnation in bank lending: the outstanding stock of bank loans to businesses declined from 19 per cent of GDP as of March 2022 to 14 per cent as of November 2023. The only corporate lending that was happening was subsidised loans under a government-sponsored programme (the so-called ‘5-7-9’ programme). Corporate lending started to gradually revive only in the second half of 2023. In the meantime, banks accumulated massive amounts of liquidity sitting in the central bank – 720 billion Ukrainian Hryvni (17,6 billion Euro) as of February 2024.

The high-interest rates on liquidity also discouraged banks from investing in government bonds. After the rate increase, banks almost stopped buying government bonds in the summer of 2022. The central bank had strongly encouraged the Ministry of Finance to increase rates on government bonds. These rates eventually increased from 10.3 per cent in May 2022 to 17.3 per cent by the end of 2022 and were in the vicinity of 19 per cent for most of 2023 (see the chart). Consequently, the government faced a much higher cost of servicing its domestic debt: in 2023, it spent 200 billion UAH (3.6 per cent of GDP) on interest payments on its domestic bonds.

The policy of high remuneration for bank liquidity also led to a substantial reduction in the amount of central bank profits that was transferred to state budget. In 2023, banks received 92 billion Ukrainian Hryvni (2.3 billion Euro) of income from deposit certificates, the equivalent of 1.7 per cent of GDP. This is what could have been the government income. After the deposit certificates became a matter of public discussion, the central bank introduced a windfall profit tax of 50 per cent on banks’ excessive profits, which they had to pay on their 2023 profits. This is a welcome step, but stopping the whole scheme of liquidity remuneration would be a much better solution.

The biggest elephant in the room, however, is the monetary financing of the deficit. In Ukrainian policy circles, it is taboo, not without pressure from foreign partners, notably the IMF. During the first months of the war, the NBU did such financing but stopped as soon as foreign aid started coming. It is not quite understandable why Ukraine is discouraged from using monetary financing when it was widely used by other countries when they fought wars (for example, the UK, during the Second World War, had 61 per cent of its budget financed this way). The usual objection is that it can be inflationary or lead to devaluation. Yet, there are answers to that: Singapore, for example, learning from the Keynesian policies deployed in the UK during and after WW2, has established a very effective system that allows for monetary deficit financing without currency destabilisation (see the article of Artem Gergun).

To sum up, there is lots of room for finding domestic resources for financing the war and reinvigoration of the economy. For that, the central bank should be on board with the war effort and should:

- end exorbitant rates on bank liquidity,

- stimulate the credit flow in the economy, especially to the military production sector (for example, by reducing interest rates),

- help reduce the interest rate on government bonds,

- do monetary financing of the government deficit. This could be targeted financing of defence industries and should be accompanied by smart liquidity-absorbing policies.

The Ukrainian policy space is very charged now, as the economic needs of the war are not being fulfilled. President Volodymyr Zelensky has questioned the possibility of mobilising an additional 500,000 soldiers, as the army had requested, which would cost circa 700 billion UAH. The ambition of the military to switch to a high-tech war also requires substantial financing. Ukraine has come to a point where it cannot successfully wage a war if it does not switch its economy into war mode.

Photo credits: Shutterstock.com/Skorzewiak

Find all related Progressive Post

Progressive Post